North Dakota Township Officers Association - Oil and Gas Gross Production Tax

Oil and Gas Gross Production Tax

THIS PAGE IS UNDER CONSTRUCTION

NDCC 57-51 Oil and Gas Gross Production Tax

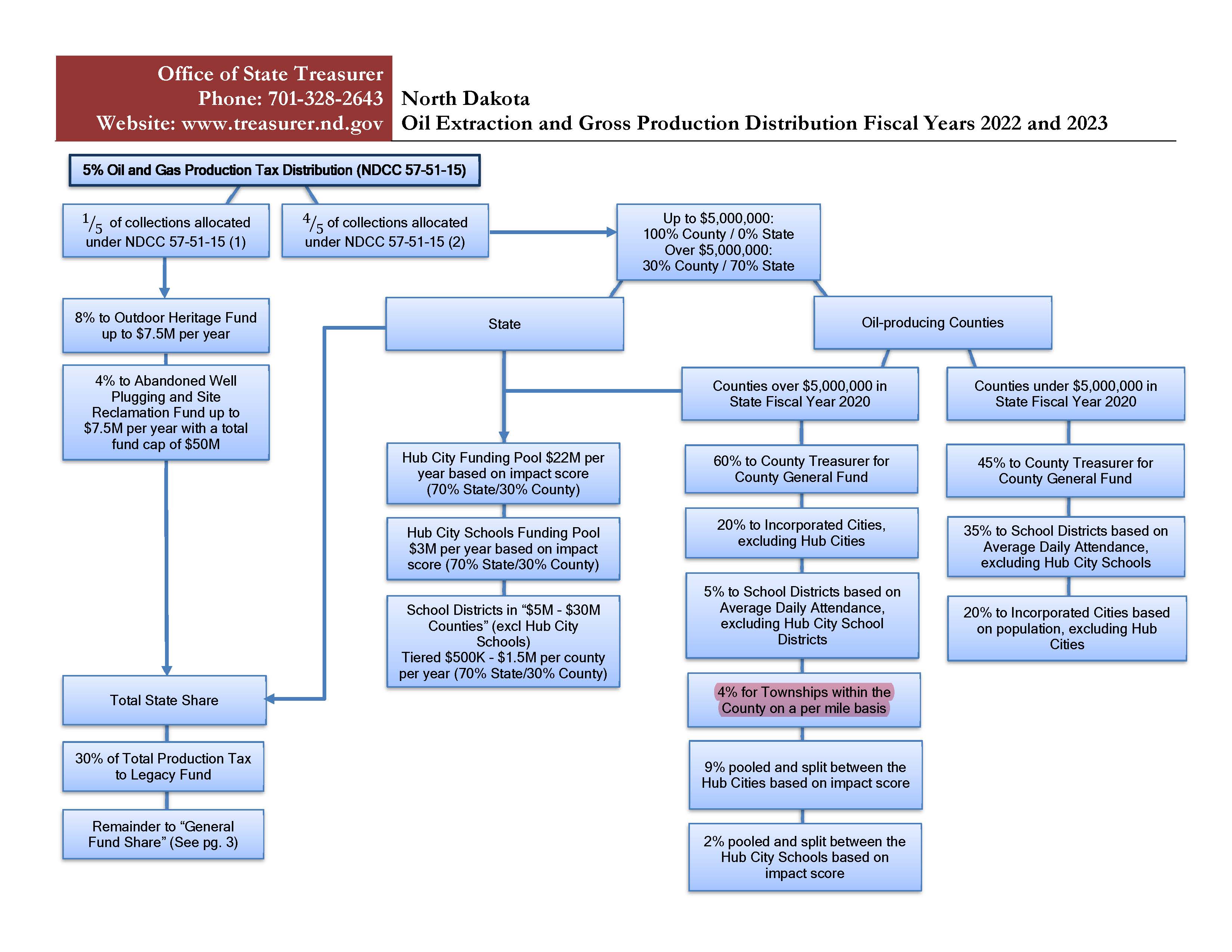

Beginning in September of 2013 (as part of 2013 HB 1358), townships in the counties that receive over $5 million of oil and gas Gross Production Tax began receiving monthly distributions through the O&G Gross Production Distribution formula.

NOTE: Funding to Oil and Gas Counties and Townships originates from 57-51 Gross Production Taxes; The funds distributed by "Operation Prairie Dog" to non-oil counties and townships originate from 57-51.1 the Extraction Tax.

NDCC 57-51-15 Oil and Gas Tax Distribution:

57-51-03. Gross production tax to be in lieu of other taxes. The payment of the taxes herein imposed must be in full, and in lieu of all ad valorem taxes by the state, counties, cities, towns, townships, school districts, and other municipalities, upon any property rights attached to or inherent in the right to producing oil or gas, upon producing oil or gas leases, upon machinery, appliances, and equipment used in and around any well producing oil or gas and actually used in the operation of such well, and also upon oil and gas produced in the state upon which gross production taxes have been paid, and upon any investment in any such property. Any interest in the land, other than that herein enumerated, must be assessed and taxed as other property within the taxing district in which such property is situated. It is expressly provided that the gross production tax is not in lieu of income taxes nor excise taxes upon the sale of oil and gas products at retail.